Why is it important to understand Evidence Based Investing?

At Evidence Based Investing, LLC, our passion is helping clients understand how free markets work and to provide them with the tools and information necessary to become smarter investors.

Evidence-Based Investing, LLC is significantly different from what is heard on Wall Street and in the financial media. Much of the investment community is focused on forecasting and predicting what will happen in the future. Their investment philosophy is based on stock picking, market timing, or past-performance investing. We focus on utilizing the science of investing and harnessing the power of the capital markets. Our decisions are based upon decades of academic research and statistical evidence. Because our investment approach is different, it is crucial to understand why we recommend it. Knowledge is the key to discipline, and without it, an investor doesn’t stand a chance of reaching their financial goals. Therefore, the following are three key concepts at the foundation of our investment philosophy and advice. We call it the Free Market Portfolio Theory.

Free Markets Are Efficient

This belief is based on the EFFICIENT MARKET HYPOTHESIS first explained by Eugene F. Fama in his 1965 doctorate thesis.

“An efficient market is defined as a market where there are large numbers of rational profit-maximizers actively competing, with each trying to predict future market values of individual securities, and where important current information is almost freely available to all participants. In an efficient market, competition among the many intelligent participants leads to a situation where, at any point in time, actual prices of individual securities already reflect the effects of information based both on events that have already occurred and on events which, as of now, the market expects to take place in the future. In other words, in an efficient market at any point in time the actual price of a security will be a good estimate of its intrinsic value.” Eugene F. Fama, “Random Walks in Stock Market Prices,” Financial Analysts Journal, September/October 1965.

What this means:

All available information is factored into the current price, and therefore, only new, unknowable information and events change pricing. Based on supply and demand, the market is the best determinant of price. Thus, attempting to consistently predict market movements and capturing additional returns unrelated to risk is not possible for any individual or entity.

- We focus on capturing market returns as opposed to trying to beat it. There is overwhelming evidence that the vast majority of fund managers fail to beat the index. Why pay the higher management fees to achieve a lower than market return and even worse, increase overall risk?

- We utilize asset-class or structured funds. These are the same type of funds utilized by institutional investors. These funds offer many of the positive attributes of an index but remove the disadvantages inherent in how they are constrained.

- We diversify prudently based upon evidence and correlation indices.

- We eliminate stock picking, track record investing, and market timing from the process.

Risk and Expected Return Are Related

The second basic component of our investment philosophy is MODERN PORTFOLIO THEORY, which earned the Nobel Prize in Economics in 1990 for the collaborative work of Harry Markowitz, Merton Miller, and Myron Scholes.

What this means

Investors who expect or need to achieve higher returns must accept the associated risks. Stock-like returns do not come without appropriate risks. When it comes to investing, there’s no “free lunch”; there is no promise of higher returns without higher risk. Anyone who tells you different is peddling a “free meal” you don’t want to eat.

- The risk of an individual asset is far less important than the contribution the asset makes to the portfolio’s risk as a whole.

- For the same amount of risk, diversification can increase returns.

- The mechanism to reduce risk is dissimilar to price movements; therefore, the task is to find assets with low correlations.

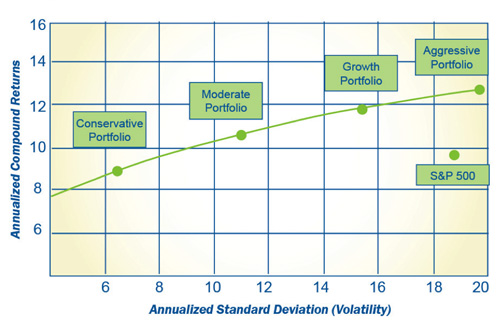

- The Efficient Frontier measures an individuals expected return given a specific amount of risk (volatility).

Graph of Markowitz’s Efficient Frontier

All Risks Are Not Created Equal

The final component of the Free Market Portfolio Theory is the THREE-FACTOR MODEL, which defines three independent dimensions of equity returns. Until recently, much of investing involved guessing what really matters in returns. In 1991 Eugene F Fama and Kenneth R. French, two leading economists, conducted an exhausted investigation into the source of risk and return. Grounded in Efficient Market Hypothesis, their research revealed that a portfolio’s exposure to three simple but diverse risk factors determines the vast majority of investment results. These three factors are referred to as the THREE-FACTOR MODEL.

Three-Factor Model (A Summary)

* There are three independent dimensions of equity returns.

* It is possible to apply these factors to measure the role of each factor in returns.

The 3 Factors are:

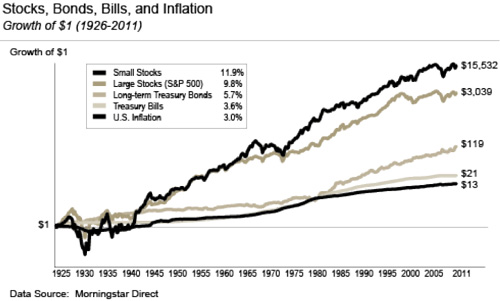

1) The Market Effect: Stocks (Equities) outperform fixed income.

- In order to achieve long term capital growth, you have to be in Equities.

- The purpose of fixed income is to soften the ride (volatility), keeping investors within their tolerance level for risk.

- Fixed income historically does not outperform inflation after taxes. It slowly diminishes your purchasing power.

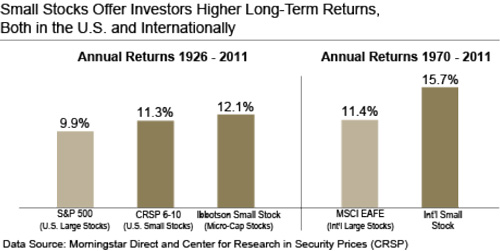

2) The Size Effect: Small cap stocks outperform large cap stocks.

- Small Cap” stocks refer to ownership of public companies with a market value (or capitalization) that is small compared to the universe of stocks.

- There is no way to capture overall stock market returns without paying close attention to small stocks since they account for most U.S. stocks.

- Small stocks are more volatile than large stocks (i.e., S&P 500), but have had higher historical returns both domestically and internationally (see chart).

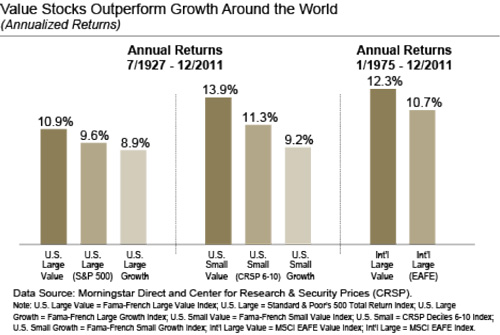

3) The Value Effect: Value stocks outperform growth stocks.

Value stocks are generally thought to be a bargain: the price is low relative to company assets, sales, and earning potential.

- Since 1927, value stocks have outperformed growth stocks (see chart).

- Given this historical superiority, you might be tempted to invest exclusively in value, but there have been periods of time, such as the late 1990s, when growth stocks outperformed value stocks by a wide margin.

- So, while value stocks are preferable, an asset mix that includes both value and growth provides the diversification necessary to reduce risk.

What this means

- It is possible to identify the sources of risk that will compensate you with premium returns.

- You need to decide how much of each type of risk you are willing to tolerate. You must structure your portfolio to achieve risk exposures in the most effective manner.

- It clarifies decisions because portfolios are based on research and rational expectations rather than hunches or predictions of the future.

Together these concepts form a powerful, disciplined and diversified approach to investing. The result is globally diversified portfolios including over 12,000 equities, using 19 distinct categories, spread across, 45 different countries, designed and engineered to capture market rates of return over specific time horizons.